Choosing the right car involves more than just looks and features; it’s also about smart financial decisions. One significant ongoing cost of car ownership is auto insurance. But did you know that the type of car you drive can heavily influence your insurance premiums? If you’re looking to minimize your car insurance expenses, understanding which vehicles are the “Cheapest Insurance Cars” is a crucial first step.

According to our extensive research, Subaru stands out as the brand offering the cheapest cars to insure, averaging around $2,224 per year or $185 per month for full coverage. Following closely behind are brands like Ford, Honda, and Toyota, all known for their reliability and affordability when it comes to insurance. Interestingly, SUVs have emerged as the vehicle type with the most budget-friendly insurance rates.

This article, brought to you by the auto repair experts at mercedesbenzxentrysoftwaresubscription.store, delves into the world of affordable car insurance. We’ll break down which car makes and models are the cheapest to insure in 2024, explore the factors that contribute to these lower rates, and provide actionable tips to help you secure the most affordable car insurance possible. Whether you’re a seasoned car owner or a first-time buyer, understanding the dynamics of car insurance costs can save you significant money in the long run.

Compare Car Insurance Rates

Get matched with a top provider and compare instant quotes in just a few clicks

With one of our trusted comparison partners

Cheapest Car Brands for Insurance in 2024

Our research indicates that when it comes to brand affordability for car insurance, Subaru leads the pack. If you’re seeking the cheapest insurance cars, starting your search with Subaru, Ford, and Honda models is a smart strategy. These brands consistently demonstrate lower average insurance costs compared to many others on the market.

To give you a clear picture, the table below compares the average annual and monthly full-coverage car insurance costs for ten popular automakers. These rates are based on data for 2021-2024 models and assume a driver profile of a 35-year-old with a clean driving record and good credit – factors that generally qualify for lower premiums.

Car Insurance Costs by Automaker

| Automaker | Annual Full-Coverage Cost | Monthly Full-Coverage Cost |

|---|---|---|

| 1. Subaru | $2,224 | $185 |

| 2. Ford | $2,299 | $192 |

| 3. Honda | $2,395 | $200 |

| 4. Toyota | $2,456 | $205 |

| 5. Chevrolet | $2,513 | $209 |

| 6. Nissan | $2,603 | $217 |

| 7. Hyundai | $2,625 | $219 |

| 8. Kia | $2,721 | $227 |

| 9. GMC | $3,062 | $255 |

| 10. Tesla | $4,098 | $342 |

This data clearly illustrates that brands like Subaru, Ford, Honda, and Toyota offer some of the cheapest insurance cars. Tesla, on the other hand, sits at the higher end of the spectrum, indicating significantly more expensive insurance premiums.

Top Car Models with the Cheapest Insurance in 2024

While brand averages are helpful, drilling down to specific models provides even more precise insights into finding the cheapest insurance cars. Below is a ranking of 32 car models, from the least to most expensive to insure in 2024. This list encompasses a range of vehicle types, showcasing that affordable insurance can be found across different segments.

Model-Specific Car Insurance Costs

| Vehicle Model | Annual Full-Coverage Cost | Monthly Full-Coverage Cost |

|---|---|---|

| 2021 Ford Bronco | $2,192 | $183 |

| 2021 Subaru Crosstrek | $2,214 | $185 |

| 2021 Honda CRV Hybrid | $2,223 | $185 |

| 2021 Subaru Impreza | $2,233 | $186 |

| 2021 Chevy Equinox | $2,253 | $188 |

| 2021 Ford Escape Hybrid | $2,266 | $189 |

| 2021 Kia Sportage | $2,298 | $192 |

| 2021 Toyota Rav4 | $2,325 | $194 |

| 2021 Nissan Frontier | $2,396 | $200 |

| 2021 GMC Sierra | $2,418 | $202 |

| 2021 Ford F150 | $2,438 | $203 |

| 2021 Honda Ridgeline | $2,455 | $205 |

| 2021 Chevy Silverado | $2,458 | $205 |

| 2021 Toyota Tacoma | $2,460 | $205 |

| 2021 Hyundai Santa Fe | $2,486 | $207 |

| 2021 Honda Civic | $2,507 | $209 |

| 2021 Nissan Rogue | $2,517 | $210 |

| 2021 Nissan Leaf | $2,519 | $210 |

| 2021 GMC Acadia | $2,546 | $212 |

| 2021 Toyota Prius | $2,582 | $215 |

| 2021 Chevy Malibu | $2,602 | $217 |

| 2021 Hyundai Elantra | $2,681 | $223 |

| 2021 Hyundai Ioniq | $2,709 | $226 |

| 2024 Chevy Silverado EV | $2,740 | $228 |

| 2021 Kia Forte | $2,799 | $233 |

| 2021 Nissan Altima | $2,981 | $248 |

| 2022 Kia EV6 2022 | $3,067 | $256 |

| 2021 Tesla Model Y | $3,426 | $286 |

| 2021 Tesla Model 3 | $3,664 | $305 |

| 2022 GMC Hummer EV 2022 | $4,221 | $352 |

| 2021 Tesla Model X | $4,516 | $376 |

| 2021 Tesla Model S | $4,786 | $399 |

This table reveals that the 2021 Ford Bronco is the model with the absolute cheapest car insurance in our analysis. However, several other models, particularly SUVs and hybrids from brands like Subaru, Honda, and Chevy, also offer very competitive insurance rates. Notice how models from Tesla consistently appear at the higher end, reinforcing the trend observed in the brand comparison.

Vehicle Types and Insurance Affordability

Beyond specific makes and models, the type of vehicle plays a significant role in determining insurance costs. Our research points to SUVs and hybrids as the most affordable vehicle types to insure on average.

Average Insurance Costs by Vehicle Type

| Vehicle Type | Annual Full-Coverage Cost | Monthly Full-Coverage Cost |

|---|---|---|

| SUV | $2,339 | $195 |

| Hybrid | $2,357 | $196 |

| Truck | $2,439 | $203 |

| Sedan | $2,635 | $220 |

| EV | $3,520 | $293 |

As you can see, SUVs and Hybrids generally attract lower insurance premiums than sedans, trucks, and especially electric vehicles (EVs). This is often attributed to factors like safety ratings, repair costs, and the typical driving habits associated with these vehicle categories.

Characteristics of Cars with the Cheapest Auto Insurance Rates:

Vehicles that consistently rank as the cheapest insurance cars often share several key attributes:

- Ease of Driving: Cars that are easy to handle and maneuver tend to be involved in fewer accidents.

- Standard Components: Readily available and affordable parts contribute to lower repair costs, which insurers appreciate.

- Strong Safety Performance: Vehicles with high safety ratings and advanced safety features are statistically less likely to result in serious injuries in accidents.

- Low Damage Liability: Cars that cause less damage to other vehicles in accidents can reduce the insurer’s payout in liability claims.

- Passenger Protection: Vehicles designed to protect occupants effectively in crashes are viewed favorably by insurance companies.

Key Factors Influencing Car Insurance Rates for Different Cars

Understanding why some cars are cheaper to insure than others is essential for making informed decisions. While choosing one of the models listed above is a great starting point, various factors related to the vehicle itself, your insurance choices, and your personal profile come into play.

Vehicle-Specific Factors Affecting Insurance Premiums

Even within the “cheapest insurance cars” category, specific vehicle characteristics can influence your rates:

- Vehicle Age: Contrary to common belief, newer cars aren’t always cheaper to insure. While older cars might have lower repair costs, newer cars often boast advanced safety features that can reduce accident severity and thus, insurance premiums. However, high-tech components in new cars can also lead to expensive repairs, balancing out the safety benefits.

- Vehicle Type: As highlighted earlier, vehicle type is a major determinant. SUVs and minivans generally see lower premiums, while sedans, large SUVs, pickup trucks, EVs, luxury cars, and sports cars tend to be more expensive to insure.

- Trim Level: Opting for higher trim levels with premium features often translates to higher insurance costs. These upscale features are typically more expensive to repair or replace.

- Safety Features: Vehicles with excellent safety ratings from organizations like the National Highway Traffic Safety Administration (NHTSA) and Insurance Institute for Highway Safety (IIHS) generally qualify for lower insurance. Basic safety features like airbags, anti-lock brakes, and seatbelts also contribute to reduced premiums.

- Car Theft Rates: Certain car models are unfortunately more prone to theft. The National Insurance Crime Bureau (NICB) publishes annual reports on vehicle theft, and models with high theft rates often carry higher insurance premiums to compensate for the increased risk.

Insurance Coverage Choices and Their Impact on Cost

Your decisions regarding insurance coverage levels and policy features directly impact your premiums:

- Coverage Level: Opting for state-mandated minimum liability coverage will always be cheaper than full-coverage car insurance. However, minimum coverage provides less financial protection in case of an accident.

- Deductible Amount: Choosing a higher deductible (the amount you pay out-of-pocket before insurance kicks in) will lower your monthly premiums. Conversely, lower deductibles mean higher premiums but less out-of-pocket expense after a claim.

- Policy Bundling: Many insurance companies offer discounts when you bundle your car insurance with other policies, such as homeowners or renters insurance. This can be a significant way to reduce your overall insurance costs.

- Annual Mileage: Driving less often typically translates to lower insurance rates. Insurers see lower mileage drivers as less likely to be involved in accidents due to reduced exposure on the road.

Personal Driver Profile Factors Affecting Insurance Rates

Even if you choose one of the cheapest insurance cars, your personal driving history and demographics play a crucial role in determining your final insurance premiums:

- Driving Record: A clean driving record is paramount for securing cheap car insurance. Accidents, speeding tickets, and DUIs on your record will significantly increase your rates. Insurers prioritize drivers with a history of safe driving.

- Age, Gender, and Marital Status: Statistically, younger drivers, particularly young males, and single individuals are considered higher-risk groups. As a result, they often face higher insurance premiums. Gender can also play a role, with young males sometimes paying more than young females.

- Credit Score: In many states, your credit score is a factor in car insurance pricing. A poor credit score can lead to significantly higher premiums, as insurers correlate lower credit scores with a higher likelihood of filing claims. In fact, drivers with poor credit may pay even more than those with speeding tickets or at-fault accidents.

- Location: Your geographic location matters. Living in densely populated urban areas with high crime rates, uninsured driver populations, or frequent accidents generally results in higher insurance costs compared to rural areas. Cities like New York City or Los Angeles often have higher average premiums than more sparsely populated regions.

Maintaining a good credit score and a clean driving record are key to accessing the cheapest car insurance rates, regardless of the vehicle you choose. While selecting from the list of cheapest insurance cars can lower your base premium, these personal factors remain critical determinants of your final cost.

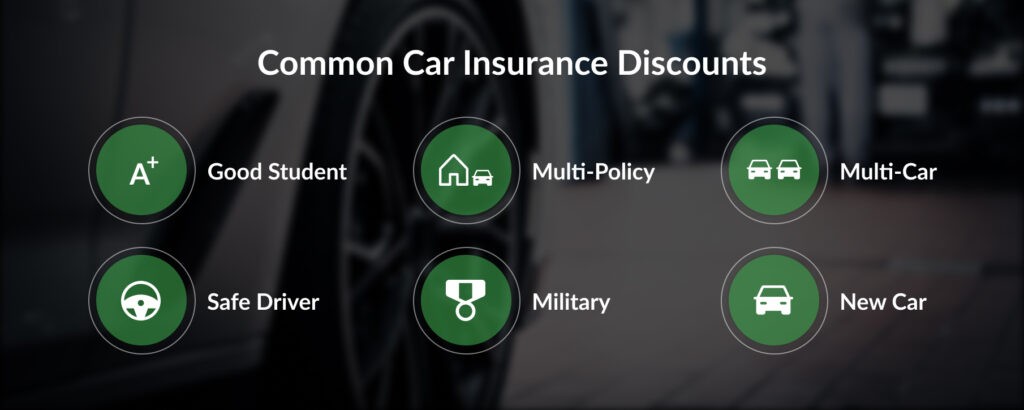

Car Insurance Discounts: Further Reducing Your Premiums

Beyond choosing the right car, exploring available car insurance discounts is another effective strategy to lower your premiums. Many insurance providers offer a variety of discounts that can add up to substantial savings.

Common Car Insurance Discounts:

| Car Insurance Discounts | Discount Details |

|---|---|

| Safe driver discount | Lower premiums for drivers with a history of accident-free driving (typically for multiple years). |

| Good student discount | Reduced rates for full-time students maintaining a B average or better. |

| Multi-vehicle discount | Savings for insuring multiple vehicles under the same auto policy. |

| Multi-policy discount | Discounts for bundling car insurance with other insurance types (homeowners, renters, etc.) from the same provider. |

| Military discount | Special rates for active-duty military personnel and veterans. |

| Vehicle safety features discount | Discounts for cars equipped with safety features like airbags, anti-lock brakes, and anti-theft systems. |

| Senior discount | Lower rates for older drivers (typically 55+) , sometimes with completion of a driving safety course. |

| Usage-based insurance discount | Premiums adjusted based on real-time driving habits tracked through telematics devices, rewarding safe driving practices. |

These are just a few examples of common car insurance discounts. To maximize your savings, it’s crucial to inquire about all available discounts when comparing quotes from different insurance providers. Every discount you qualify for directly translates to lower out-of-pocket expenses.

Is Choosing the Cheapest Insurance Car Always the Best Strategy?

While cost is undoubtedly a significant consideration, making your car purchase solely based on insurance premiums isn’t always the wisest approach. While the cheapest insurance cars are often safe and reliable, they might not perfectly align with your needs, preferences, or lifestyle. Furthermore, extremely low insurance rates from some providers could be a red flag, potentially indicating inadequate coverage or questionable business practices.

It’s crucial to strike a balance between affordability and adequate protection. While opting for minimum liability coverage will lower your premiums, it might leave you financially vulnerable in the event of a serious accident. Similarly, skipping comprehensive and collision coverage to save money means you’ll be paying out-of-pocket for damages to your own vehicle, regardless of fault.

Consider your individual circumstances, driving habits, and risk tolerance when deciding on both your car and your car insurance policy. The “cheapest insurance car” is only truly valuable if it also meets your practical needs and if the associated insurance coverage provides sufficient protection for your peace of mind.

Compare Car Insurance Rates

Get matched with a top provider and compare instant quotes in just a few clicks

With one of our trusted comparison partners

Frequently Asked Questions: Cheapest Insurance Cars

Here are answers to some common questions regarding the cheapest cars to insure:

What is the absolute cheapest car model to insure?

Our data indicates that the 2021 Ford Bronco is the cheapest model to insure in 2024, with an average full-coverage cost of approximately $2,192 annually or $183 monthly. These figures are based on a 35-year-old driver with a good driving record and credit score.

Which car insurance company offers the cheapest rates?

Geico is often cited as one of the cheapest car insurance companies nationwide. However, rates are highly personalized and vary based on individual driver profiles and locations. The best way to determine if Geico is the cheapest for you is to compare personalized quotes from Geico and other top insurers like State Farm, USAA, and Progressive.

Are newer cars always cheaper to insure?

Not necessarily. While newer cars often have advanced safety features that can lower insurance costs, the higher repair costs associated with sophisticated components in new vehicles can sometimes offset these savings, making older cars surprisingly affordable to insure in some cases.

Is it cheaper to insure an automatic or manual car?

Manual cars are typically slightly cheaper to insure than automatic cars. Automatics often have more complex and expensive transmissions to repair, which can translate to marginally higher insurance premiums.

Does the price of the car directly correlate with insurance cost?

Generally, more expensive cars are more expensive to insure due to higher repair and replacement costs. However, a less expensive car isn’t always cheaper to insure. Factors like age, make, model, safety features, and theft rates can all influence insurance premiums, sometimes making a less expensive car surprisingly costly to insure.

What types of cars are the most expensive to insure?

Luxury cars and vehicles with a higher likelihood of theft, accidents, or costly claims are generally the most expensive to insure. Sports cars, high-performance vehicles, and certain luxury SUVs often fall into this category.

Are SUVs or sedans cheaper to insure?

In 2024, our data suggests that SUVs are slightly cheaper to insure than sedans on average. This may be due to the perceived safety benefits of larger vehicles and potentially lower claim frequencies for certain SUV models.

Our Methodology: Car Insurance Rate Analysis

Our car insurance rankings and rate analyses are built on a robust and transparent methodology to ensure objectivity and accuracy. We collect data on a wide range of auto insurance providers and evaluate them based on a comprehensive set of ranking factors.

Key Ranking Factors:

- Coverage Options (30% of score): We prioritize companies that offer a broad spectrum of coverage choices to meet diverse consumer needs.

- Cost and Discounts (25% of score): We analyze car insurance rate estimates provided by Quadrant Information Services and assess the availability and value of various discount opportunities.

- Industry Standing (20% of score): Factors like market share, ratings from industry expert organizations, and the company’s years of operation are considered to gauge industry strength and reliability.

- Customer Experience (15% of score): Customer satisfaction is evaluated through complaint data from the National Association of Insurance Commissioners (NAIC), J.D. Power customer satisfaction ratings, and our own shopper analysis assessing the responsiveness and helpfulness of customer service teams.

- Availability (10% of score): Companies with wider state availability and fewer eligibility restrictions score higher, reflecting greater accessibility for consumers.

Credibility Metrics:

- 800+ hours of dedicated research

- 130+ car insurance companies thoroughly reviewed

- 8,500+ consumers surveyed to gather real-world insights

*Data accurate as of publication date.

For feedback or questions regarding this article, please contact our team at [email protected].